Let’s be honest, when it comes to personal finance…you either love it or hate it. But…

How Interest Rates Work

If you want to purchase something now but do not have the cash to spend, what you can do is to borrow it. This borrowing does have a cost though, it is called interest. It is an amount that you have to pay on top of the money you have loaned– the principal amount. The rate of interest is often expressed as an annual percentage of the principal. To illustrate, if you have borrowed $1,000 with an interest rate of 10 percent per year payable after a year, you will pay a total amount of $1100 at the end of the year. Loans can be short term or long term, hence the borrower is said to pay either short term interest rates or long term interest rates.

Interest Rates: The Key Concepts

The idea of putting an interest to a loan hinges upon several things. There are people or entities like corporations and governments that are willing to pay interest for the temporary use of the money, while there are lenders willing to give up the chance to use the money today. Banks give a small interest rate to you if you park your money with them. Government sells bonds and pays the lender a certain amount of compensation for it. At the same time, the lender needs to impose an interest because of the risk he is taking when lending as there is a possibility that the borrower may not be able to pay him back. The higher the perceived risk is, the higher the rate of interest. This is the reason why it is very important to maintain a good credit standing.

Simple versus Compound Interest Rates

Interest rates can be simple or compound. Simple interest rate, which is also called flat rate, is always taken as a percentage of the principal loan amount while a compound interest is not only calculated based on the principal but also on fees and interest amount that have already been included to the principal.

Using the above example of a $1000 loan with a 10 percent interest rate, the amount of simple interest after a year would be $100. If the principal remained unpaid for four years, for example, the interest would be $400. The borrower then owes the lender a total of $1400. Even if the loan remains unpaid for a few more years, the interest would still be computed based on the principal amount of $1000.

If the interest rate is compounded, there is an interest imposed on the interest and other fees that the lender may impose for not paying on time. The formula for calculating the amount to be paid after 4 years using the same example is:

Amount payable= Principal x (1 + Interest rate) ^number of years

If you have not paid within 4 years, your loan amounting to $1000 with an annual interest rate of 10 percent would turn into $1,464.10, higher by $64.10 than if the loan was subjected to a flat rate. Compound interest is the reason why bills grow so quickly. It is a more common type of interest rate used by banks and lending companies.

What Determines the Interest Rate You Get on Loans and Credit Cards?

You may be complaining that your savings accounts have very low interest rates and thus, putting your money in the bank is not a smart choice if your objective is to grow your money. Why do banks give paltry interest rates on your money but charge higher interest rates when you borrow? Remember that the level of interest is reflective of the risks that the lender is facing when lending. With banks, there is very low, even close to zero, risk of not paying or defaulting. Therefore, they give you a low interest rate on your return because have a very low chance of default. Your money may also most likely be covered by deposit insurance. Also, government-issued bonds provide relatively minimal interest rates because governments rarely default.

- Credit Score

One of the factors that affect interest rates is your credit standing. The better your credit score is, the lower the interest rate that a lender can give for your loan.

- Secured versus Unsecured Credit

Interest rates on credit considered as unsecured are higher than those that are categorized as secured. Credit cards fall under unsecured because you do not need collateral to secure a loan. On the other hand, a mortgage is an example of a secured loan because the house serves as the collateral. This is the reason why interest rates on credit cards are much higher than those of mortgages.

- Long-term versus Short-term Loans

Long term interest rates are also higher than short-term interest rates. A lender has to wait for a long time before he can get back the money in the case of long-term loan. Many things can also happen which can affect the value of the interest rate in the long term. Long term interest rates are also high due to the uncertainty brought by inflation. This makes long term loans less appealing to lenders. They’d rather prefer to lend on a short term basis because the money will not lose a lot of its value. With long-term loans, the interest rate can be offset by rising inflation such that at the end of the maturity period, the money’s worth would be far less than it was when the loan was taken.

Understanding Nominal versus Real Interest Rate

The following formula is how someone would go about calculating the real interest rate:

![]()

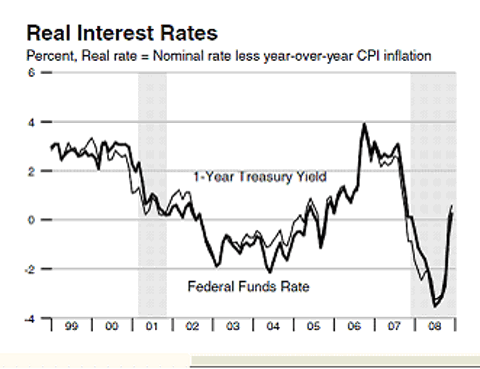

If you are lender, you have to take into account the rate of inflation and to understand the difference between nominal and real interest rate. In the above example, the 10 percent is a nominal rate. If the prevailing annual inflation rate is 3 percent, it means that you have actually imposed only 7 percent as a real interest rate. This is because even if you have gained 10 percent, your money lost 3 percent of its value; hence you get only a net of 7 percent. Therefore, you have to make sure you take into account the inflation rate when imposing an interest rate. If you think that inflation rate is likely to be higher in the future, incorporate this in your calculations. Many lending institutions re-compute their interest rates every year to account for inflation fluctuations and the overall market conditions. The chart below shows the real interest rate of the United States from 1999 to 2008. Remmeber, real interest rate equals the nominal interest rate minus inflation.

The Role of the Federal Reserve

The Federal Reserve, the United States’ central bank, is the authority that has a command over the general level of interest rates. The Fed uses interest rates as monetary policy tools to influence the economy. The Fed funds rate, for instance, is a very essential interest because it impacts the supply of money which is the health of the entire economic system.

In financial planning, it is critical to understand how interest rates work. If you are a credit card user, you should be aware of the compound interests that your lender requires you to pay. It is an everyday fact of life that you have to deal with. If you are saving and investing your money, being aware of the varying interest rates will help you make smart choices on where best to put your money.

More to Explore